Trust FAQs

The appointor (sometimes called Principal or Guardian) is the ultimate controller of a trust. The appointor has the power to appoint and remove the trustees. It is not essential that the trust has an appointor. CGW deeds will work with or without an appointor.

However, it is useful to have an appointor to change the trustee in situations such as death or insolvency of a trustee. The appointor may be an exisitng trustee, a named beneficiary or a third party.

Some trusts have an ‘independent’ appointor (such as an accountant) to reduce the risk of individual beneficiaries being held to control the trust.

We recommend against having a sole individual trustee who is also a beneficiary.

There is an argument that, where a sole trustee is also a beneficiary, all of the net income is assessable to that trustee because they have the unilateral power to retain or distribute to other beneficiaries.

While we are only aware of one occasion where the ATO has raised this as a possible issue, the prudent approach is to have joint trustees for clients who do not want a corporate trustee. If there are joint trustees then no beneficiary has unilateral power to determine how the income is distributed.

The maximum number of trustees you can have is four.

A trustee is personally liable for debts incurred on behalf of the trust and, although the trustee has the right to be indemnified out of the assets of the trust, it is usually preferable for a sole purpose company to be trustee so that the risk of trust activities is quarantined to the assets in the trust.

With individual trustees, all assets have to be transferred into the name of a new trustee if a current trustee resigns or dies. However if the trustee is a company there is no need to transfer assets if a director dies or resigns.

The costs associated with maintaining a corporate trustee are not substantial.

The directors of a trustee company can be beneficiaries in their individual capacity while still being in control of the trust.

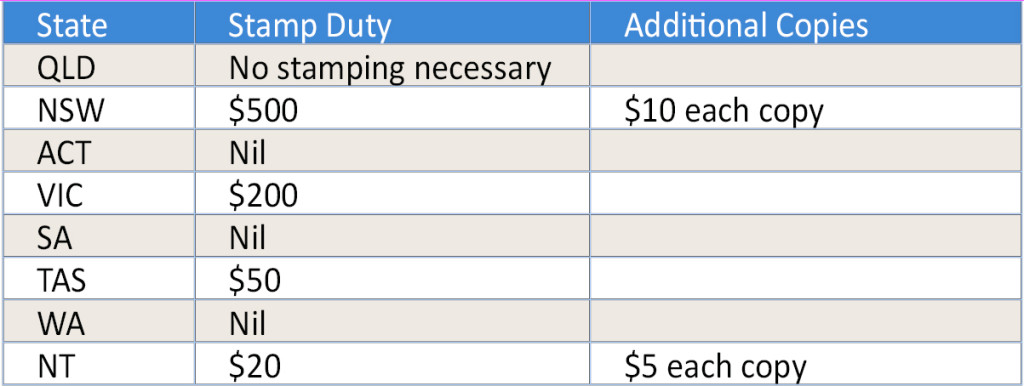

Generally, the establishment of a trust deed will be subject to either nil or nominal duty. The requirements in relation to stamping a trust deed vary from state to state. The stamping fees for discretionary and unit trusts, if by declaration/settlement of cash only are set out below:

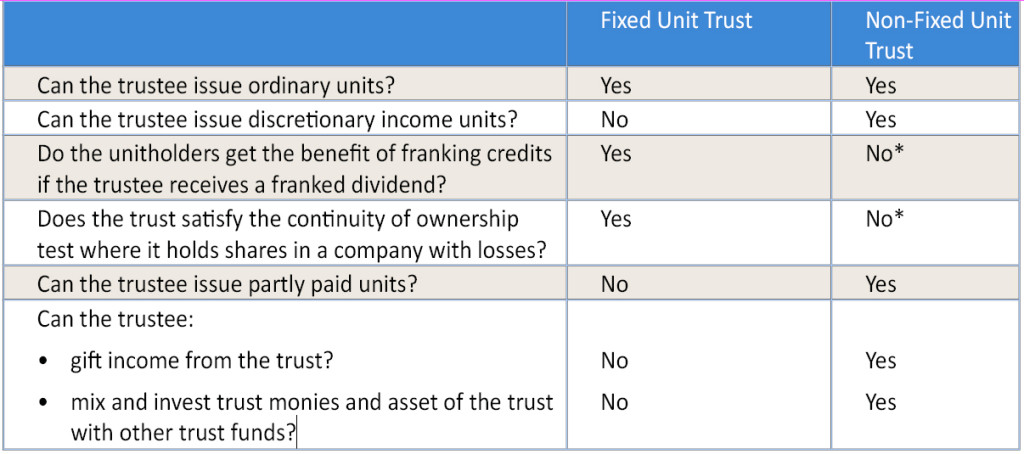

There are a number of issues you should take into account in choosing between a fixed and a non-fixed unit trust. The key differences are sumarised below:

*Unless the trust lodges a family trust election

Recent cases also highlight the fact that most private unit trusts do not meet the current criteria for a fixed trust – therefore if you have an existing unit trust deed, you may need to update it if you require the trust to be fixed.

A fixed trust is more restrictive than our ordinary unit trust, which may be a problem if there are non-arm’s length unitholders.

For example, many decisions have to be approved by a unanimous resolution of unitholders (e.g. amendments to the trust deed).

Recent cases also indicate that, unless unit redemptions and issues have to be based on a valuation determined on a net asset basis and in accordance with Australian accounting principles, the unitholders may not have a fixed entitlement.

While we do not agree with the recent case law, it is likely the ATO will seek to take this valuation position and therefore the safest option is to include these valuation methods in the unit trust deed.

The deed can be amended in future (by unanimous consent) if an alternative valuation method is agreed.

A direct descendants trust deed contains provisions which prohibit capital distributions to anyone other than a direct descendant of the initial clients unless the initial clients consent.

This deed may be attractive to clients who have concerns about sons or daughters-in-law or other third parties (e.g. trustee in bankruptcy) accessing the trust capital.

However, the trust has the usual wide range of income beneficiaries so the clients still have substantial flexibility for tax planning purposes.